The Bangladesh government and the central bank have implemented a series of initiatives to keep the foreign currency reserves from falling further, a trend which is putting an increasing amount of strain on the country’s economy.

As part of these measures, the National Board of Revenue (NBR) – in a circular on Tuesday – slapped additional taxes on imports of luxurious and non-essential items, in a bid to counter the ongoing depletion of forex reserves.

Meanwhile, the Bangladesh Bank on Monday relaxed the requirement for availing cash incentive on remittance, a move which would help increase the flow of remittance in the country.

Bangladeshi expatriates now can get this incentive without submitting any documents, read a central bank notice.

On Sunday, the banking regulator imposed restrictions on bank officials and employees on traveling abroad to safeguard forex reserves.

The same day, the government decided to prepare a list of products to suspend their imports amid the forex crisis, insiders told The Business Post, adding that the list has not been completed as yet.

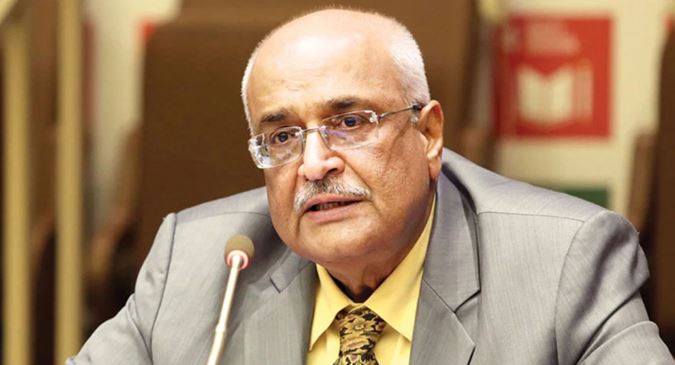

Bangladesh Bank Executive Director and spokesperson Md Serajul Islam said, “The bankers’ personal trips abroad have been restricted due to the present unfavourable economic situation in home, and turbulent global economy.

“We will take every step necessary in the coming days to protect our forex reserves for dipping further.”

On May 10, the central bank toughened its rules for luxury item imports. A day later, the government decided to stop foreign trips of its officials and postponed the implementation of less important projects that require imports.

On May 16, the Finance Division said the employees of autonomous, state-owned, semi-government organisations and state-owned banks and financial institutions cannot go on overseas trips, which would help Bangladesh maintain a stable foreign exchange reserve.

BB to meet with bankers soon

Bangladesh Bank officials are planning to organise a meeting with bankers as soon as possible to discuss the volatility in the foreign exchange market, said a senior official of the central bank.

The Bangladesh Foreign Exchange Dealers’ Association (BAFEDA) recently submitted a six-point proposal to the central bank for stabilising the country’s forex market.

It recommended increasing cash incentives against wage earners’ remittance to 5 per cent from existing 2.5 per cent, proposed a periodic review of the inter-bank exchange rates, and requested necessary adjustments based on market dynamics.

According to the central bank, Bangladesh’s forex reserves stood at $42.32 billion last Thursday, down from $46.15 billion recorded on December 31, 2021.

Economists say the country’s forex reserves are declining mainly due to the growing import payments amid the Russia-Ukraine war and economic recovery from the Covid-19 pandemic.

The settlement of letters of credit (LCs), also known as actual import payment, rose by 49.66 per cent to $61 billion during July to March this fiscal year, central bank data shows.

Growing import payments have put pressure on the foreign exchange market. As a result, the local currency lost its value by 3.65 percent in the last ten months, despite the injection of USD by the central bank.

The inter-bank exchange rate stood at Tk 87.90 per USD on Monday, up from Tk 87.50 on Sunday. Prior to that, THE central bank devalued taka by 80 paisa against the USD on May 16, the highest depreciation of the local currency in a single day.

From August till this Tuesday, the Bangladesh Bank has injected more than $5 billion in the banking industry.

A very tough time

Bankers and economists have welcomed the government’s initiatives to protect the foreign currency reserve.

“The government and the central bank have taken timely initiatives, as this is a very tough time,” Mutual Trust Bank’s Managing Director Syed Mahbubur Rahman told The Business Post.

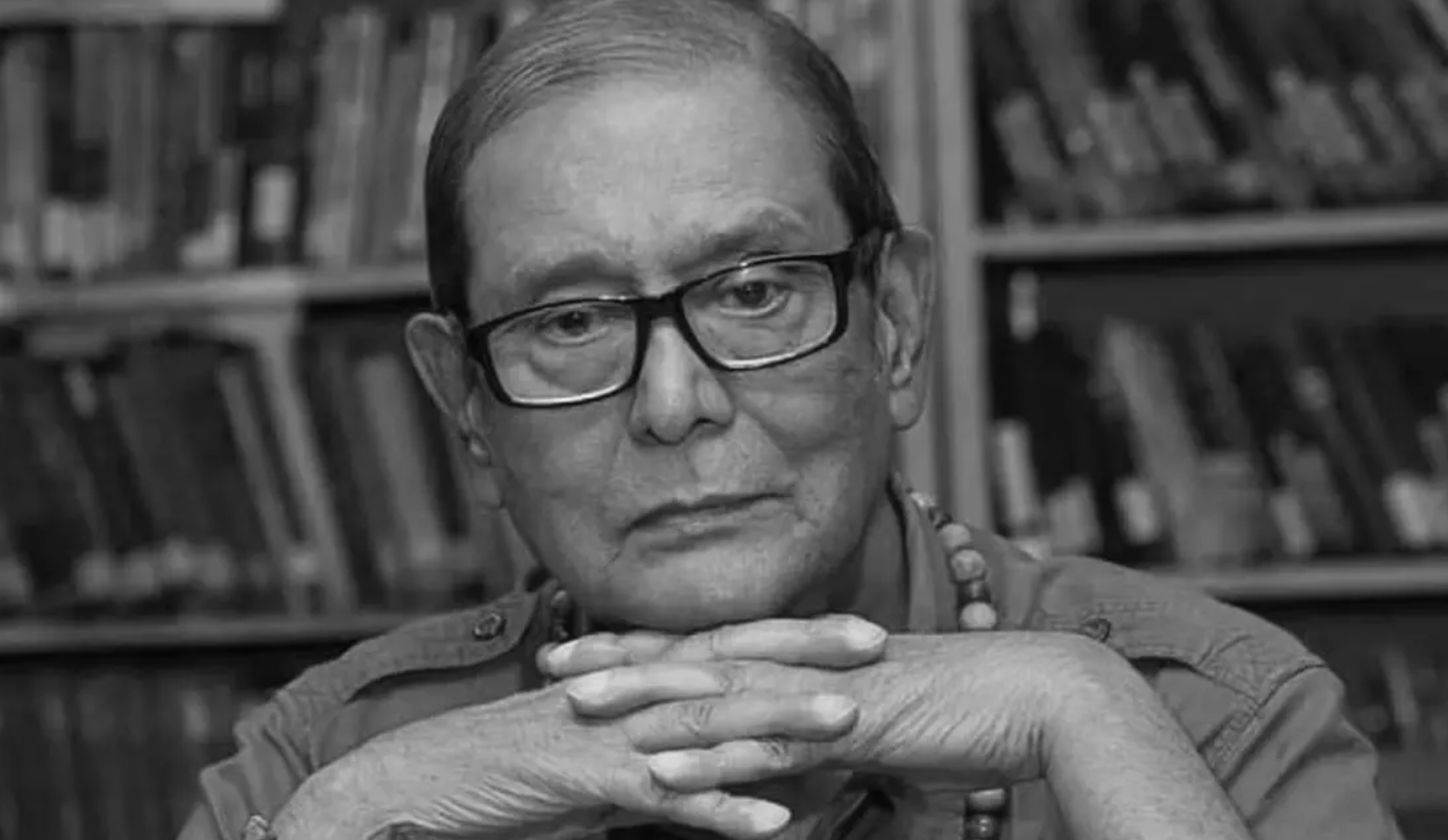

Meanwhile, former governor of the Bangladesh Bank Salehuddin Ahmed said, “The volatility of the forex market not only affected Bangladesh, but also the whole world owing to the Russia-Ukraine war and the reopening of the global economy after the Covid-19 pandemic.

“The central bank has taken measures to tackle the situation, but it is already too late. The regulator should have depreciated the local currency much earlier like many other countries.”